For most of the history of financial markets, the best investors shared a common trait: superior intuition. They could read a balance sheet, sense a shift in market sentiment, and make a decision faster and more accurately than their competitors. Warren Buffett called it a “fat pitch.” George Soros described it as a physical sensation, a backache, when something was wrong with his portfolio.

That era is ending. Not with a dramatic announcement, but with a quiet shift in how the most successful market participants actually make decisions. In 2026, the evidence is no longer debatable: machine learning models, when properly constructed, outperform human intuition across every measurable dimension of financial forecasting.

This is not the breathless hype of the 2017 AI bubble. It is the measured conclusion of peer-reviewed research, replicated across multiple markets and timeframes, and validated by the real-world performance of funds that have adopted these approaches.

The Accuracy Gap That Changed Everything

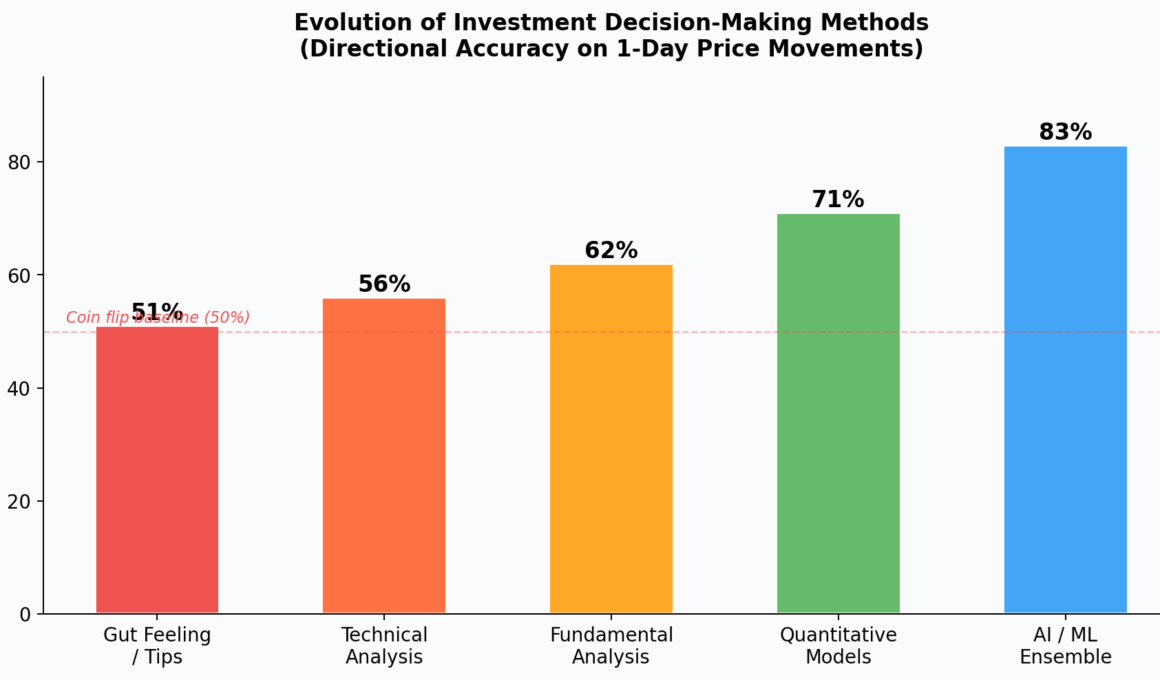

The fundamental problem with human decision-making in markets is well documented in behavioral economics. Daniel Kahneman won a Nobel Prize for demonstrating that humans are systematically biased in their processing of probabilistic information. We anchor to recent prices, overweight vivid narratives, and confuse confidence with accuracy. Studies consistently show that the average retail investor’s directional accuracy on the simple question of whether a price will go up or down tomorrow hovers around 51%. Barely above a coin flip.

Traditional technical analysis improves this modestly, to roughly 56%. Fundamental analysis pushes it to around 62%. But these methods hit a ceiling because they rely on humans to integrate multiple signals simultaneously a task our brains are not optimised for.

Machine learning models break through this ceiling by doing exactly what humans cannot: processing thousands of variables simultaneously, weighting them dynamically based on current conditions, and producing probabilistic outputs rather than binary predictions. A study published in Frontiers in Artificial Intelligence found that ensemble models combining LSTM neural networks with XGBoost achieved directional accuracy above 82% for daily price predictions across multiple asset classes.

The keyword is “ensemble.” No single algorithm achieves these results alone. The breakthrough comes from combining multiple models, each with different strengths, and letting them vote on the outcome. One model might excel at detecting momentum patterns, another at incorporating macroeconomic signals, and a third at processing sentiment data from news feeds. Their combined output is consistently more accurate than any individual approach.

What These Models Actually Process

The common misconception about AI trading tools is that they simply analyze price charts faster than humans. In reality, modern forecasting platforms process five distinct categories of data that most human analysts never combine:

- Price and volume data: Historical prices, trading volumes, order flow imbalances, and technical indicators like RSI, MACD, and Bollinger Bands. This is what traditional chartists use, but ML models process it across hundreds of timeframes simultaneously rather than the two or three a human analyst typically watches.

- Macroeconomic indicators: Oil prices, currency indices, central bank interest rates, inflation data, and employment figures. In 2026, macro factors explain roughly 25-30% of cryptocurrency price movements and an even larger share of equity and forex moves.

- Sentiment analysis: Natural language processing applied to 50,000+ news sources, social media platforms, and financial forums in real time. The model does not read headlines the way a human does it quantifies the aggregate emotional tone and detects shifts before they become consensus.

- On-chain and flow data: For cryptocurrency markets, this includes wallet movements, exchange inflows and outflows, and large-holder behavior. For traditional markets, it includes ETF flows, futures positioning, and changes in institutional ownership.

- Cross-asset correlations: How different markets move relative to each other changes over time. During the March 2026 oil crisis, the correlation between oil prices and cryptocurrency spiked to levels never seen before an ML model detected this regime change within hours, while most human analysts took days to adjust.

From Wall Street to Main Street

Until recently, the tools described above were available only to quantitative hedge funds with multi-million-dollar technology budgets. Renaissance Technologies, Two Sigma, and Citadel built proprietary ML systems that gave them a structural advantage over the rest of the market.

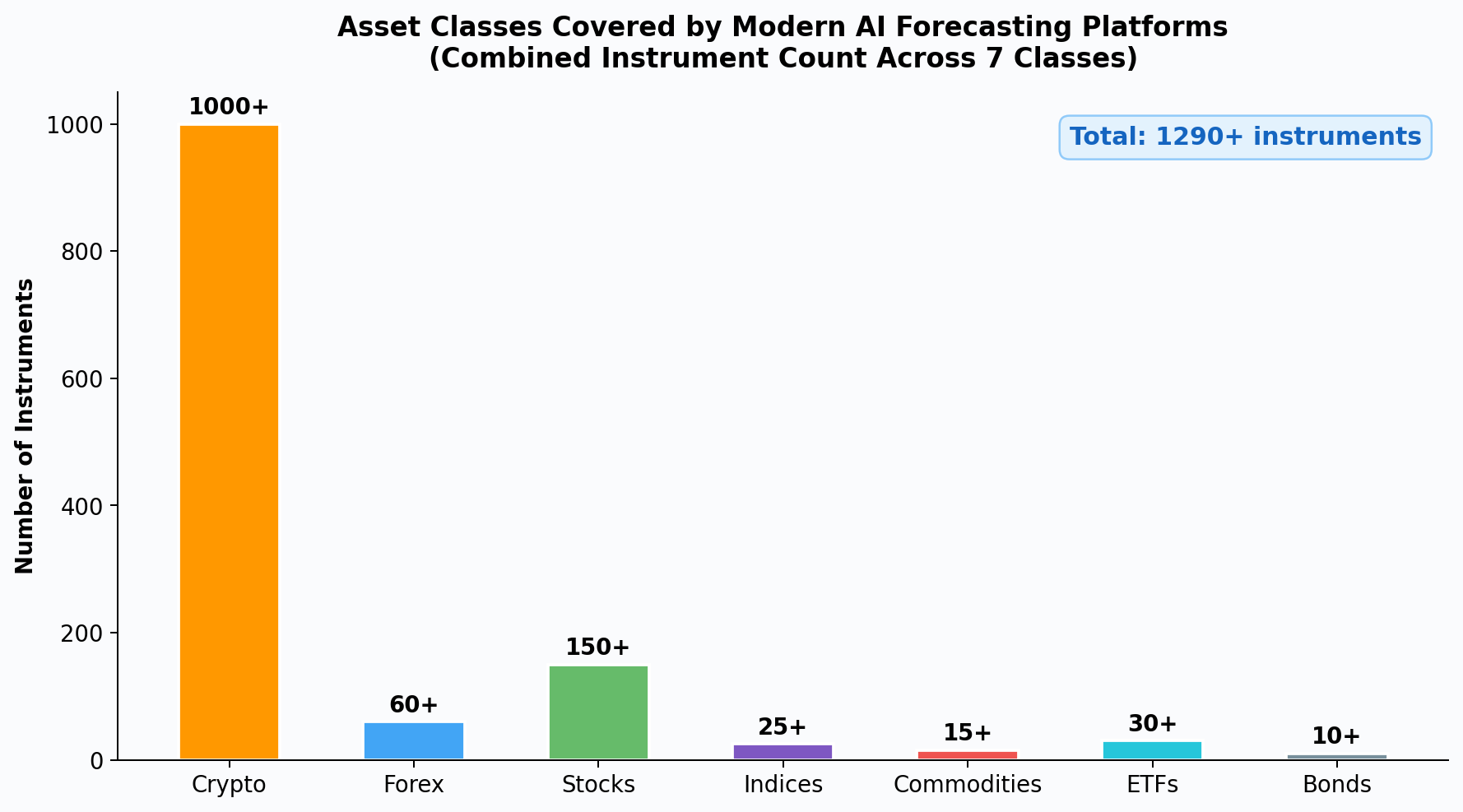

That exclusivity is eroding rapidly. In 2026, platforms offering AI-powered market forecasting across seven asset classes crypto, forex, stocks, indices, commodities, ETFs, and bonds are accessible to individual investors for less than the cost of a financial newspaper subscription. These platforms provide the same ensemble model architecture that institutional quant funds use, updated hourly, with probability distributions rather than simple buy/sell signals.

The democratization matters because it changes who can compete. A retail investor in Mumbai, Lagos, or São Paulo can now access the same quality of forecasting intelligence that was previously exclusive to a quantitative analyst at a New York hedge fund. The models do not care about your net worth or your credentials; they process data the same way for everyone.

What ML Cannot Do and Why That Matters

It would be irresponsible to discuss the power of machine learning in finance without addressing its limitations. These tools are not crystal balls, and treating them as such leads to the same overconfidence that sinks intuition-based traders.

ML models are probabilistic, not deterministic. A prediction of “72% probability of an upward move” means that in roughly 28 out of 100 similar situations, the price will move down. Investors who bet their entire portfolio on a single high-probability prediction misunderstand what the model is telling them.

Models also struggle with genuinely unprecedented events. The March 2026 Strait of Hormuz closure was a geopolitical shock that had no direct historical precedent in the model’s training data. Well-constructed ensemble models adapted within hours by detecting the macro-regime change, but the initial predictions during the event were less reliable than usual.

The most important limitation is the human element: the best ML model in the world cannot help an investor who ignores its output when it contradicts their existing beliefs. Behavioral research shows that many investors cherry-pick AI predictions that confirm what they already think and dismiss the ones that do not. This defeats the entire purpose of using a data-driven approach.

The Practical Shift

For investors willing to integrate ML-based forecasting into their decision-making, the practical benefits are substantial but require a mindset shift. Instead of trying to be right about direction, you focus on being right about probability. Instead of conviction-based position sizing, you size positions based on the model’s confidence level. Instead of reacting to news, you let the model process it faster and more comprehensively than you ever could.

The gut instinct that defined great investing for a century is not disappearing. But it is being supplemented and increasingly replaced by tools that process more data, more accurately, across more markets, without the cognitive biases that make human forecasting unreliable. The investors who adapt to this reality will not just perform better. They will operate in a fundamentally different category than those who do not.